Modern Portfolio Theory

Modern Portfolio Theory, associated with Harry Markowitz, explains how to construct portfolios that maximize expected return for a given level of risk.

Assumptions

- Investors like higher expected returns and dislike higher volatility.

- They care about the expected return and volatility of the overall portfolio.

- Investors are generally assumed to hold well-diversified portfolios.

The key questions are:

- How does each asset contribute to the risk and return of the portfolio?

- How should portfolio weights be chosen to optimize the risk-reward trade-off?

Individual Asset Properties

\[ \mu_i = \mathbb{E}[R_i], \qquad \sigma_i^2 = \mathbb{E}\big[(R_i-\mu_i)^2\big], \qquad \sigma_i = \sqrt{\operatorname{Var}(R_i)} \]

Portfolio Properties

\[ R_p = w_1R_1 + w_2R_2 + \cdots + w_nR_n \]

\[ \mathbb{E}[R_p] = w_1\mu_1 + w_2\mu_2 + \cdots + w_n\mu_n \]

Expected portfolio return is a weighted average of individual expected returns, but portfolio risk is not a simple weighted average of individual volatilities.

Unlike returns, portfolio risk depends not just on how risky the individual assets are, but on how they move relative to one another.

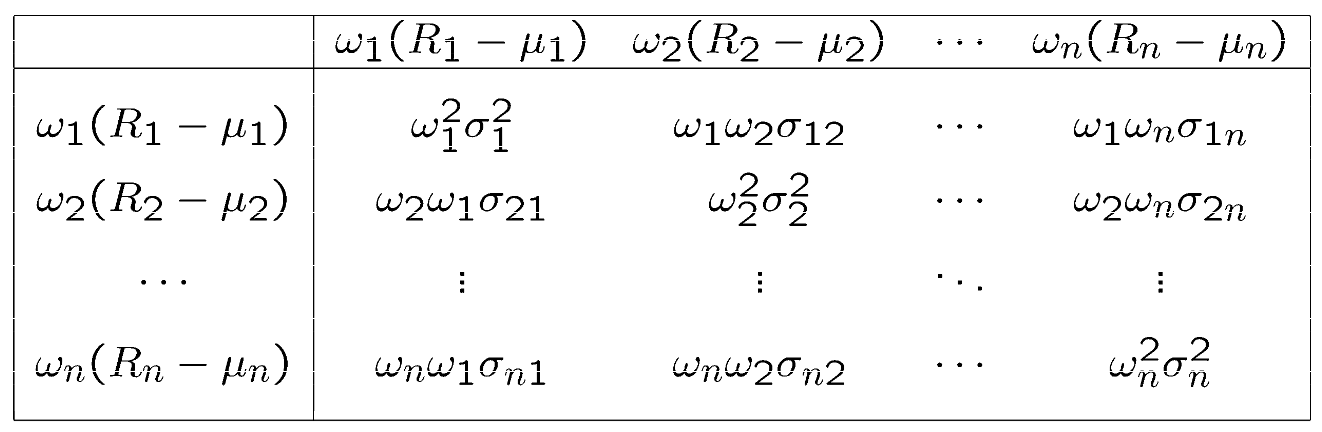

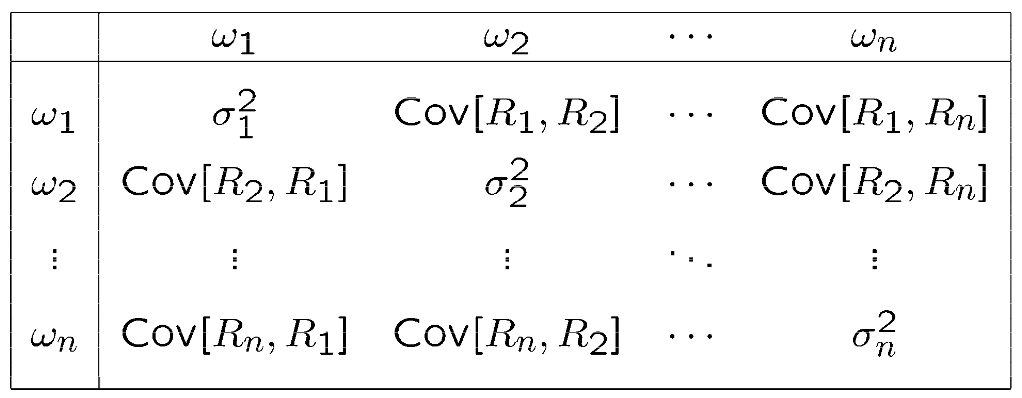

Portfolio Variance and Covariance

\[ \operatorname{Var}(R_p) = \mathbb{E}\big[(R_p-\mu_p)^2\big] \]

If we substitute the weighted-average expression for \(R_p\), we obtain

\[ \operatorname{Var}(R_p) = \mathbb{E}\Big[\big(w_1(R_1-\mu_1)+w_2(R_2-\mu_2)+\cdots+w_n(R_n-\mu_n)\big)^2\Big] \]

When we square the weighted sum of deviations, we generate cross terms. These are covariance terms.

\[ \operatorname{Cov}(R_i,R_j) = \mathbb{E}\big[(R_i-\mu_i)(R_j-\mu_j)\big] \]

\[ \mathbb{E}\big[w_i(R_i-\mu_i)w_j(R_j-\mu_j)\big] = w_iw_j\operatorname{Cov}(R_i,R_j) = w_iw_j\sigma_i\sigma_j\rho_{ij} \]

\[ \operatorname{Var}(R_p) = \sum_{i=1}^{n} w_i^2 \sigma_i^2 + \sum_{i \neq j} w_i w_j \operatorname{Cov}(R_i,R_j) \]

- Positive covariance increases portfolio variance.

- Negative covariance reduces portfolio variance.

- Diversification comes from imperfect correlation across assets.

- Off-Diagonal Terms \((\omega_i \omega_j \sigma_{ij})\) = the covariances (interactions) between assets. There are \(n^2-n\) of these terms.

In a 2-stock portfolio there are 2 variance terms and 2 covariance terms; in a 100-stock portfolio there are 100 variance terms and 9,900 covariance terms.

In the portfolio-variance matrix, diagonal terms are individual variances, while off-diagonal terms are the covariances that capture how assets interact.

As the number of assets increases, the covariance terms grow much faster than the variance terms. In large portfolios, total risk is driven mostly by covariance rather than by stand-alone volatility.