Capital Asset Pricing Model

Beta

Beta measures the sensitivity of a stock's return to the market portfolio:

\[ \beta_i = \frac{\operatorname{Cov}(R_i,R_M)}{\operatorname{Var}(R_M)} \]

Sharpe--Lintner CAPM

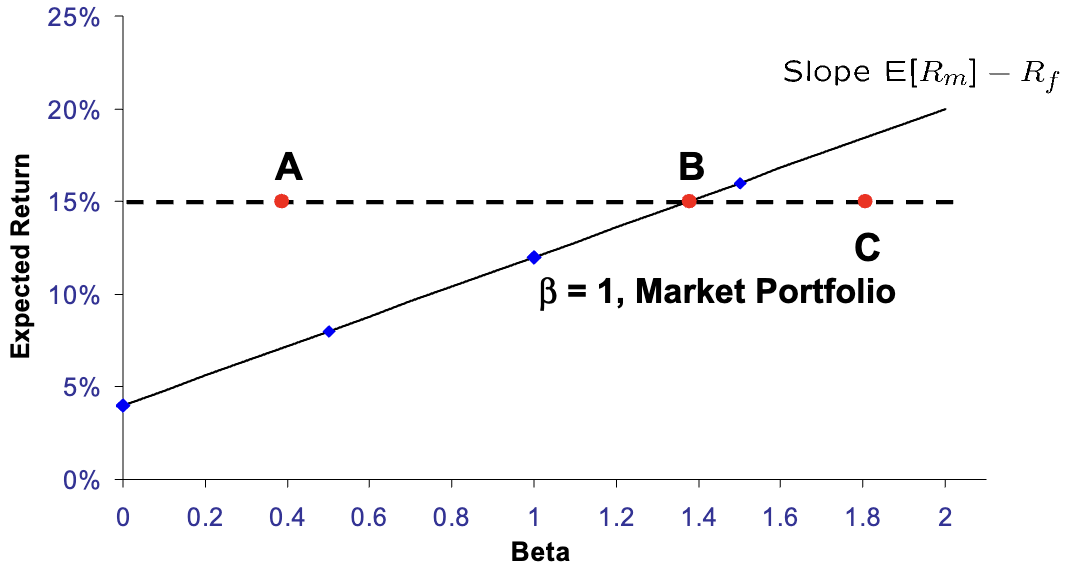

\[ \mathbb{E}[R_i] = r_f + \beta_i\big(\mathbb{E}[R_M] - r_f\big) \]

The CAPM therefore implies that the relation between expected return and priced risk is linear.

- The risk--return relation is linear.

- Beta, not total volatility, is the relevant priced risk measure.

Portfolio Beta

\[ \beta_P = \frac{\operatorname{Cov}(R_P,R_M)}{\operatorname{Var}(R_M)} = w_1\beta_1 + \cdots + w_n\beta_n \]

\[ \mathbb{E}[R_P] = r_f + \beta_P\big(\mathbb{E}[R_M] - r_f\big) \]

CAPM Assumptions

- Investors choose portfolios using expected returns and variances.

- All investors share the same estimates of means, variances, and covariances.

- There are no taxes, no transaction costs, and no short-sale restrictions.

- Investors can borrow and lend at the same risk-free rate.

- The supply of assets is fixed.

Security Market Line and Capital Market Line

Under the CAPM, correctly priced securities lie on the Security Market Line. The Capital Market Line is the line joining the risk-free asset to the market portfolio in mean--standard deviation space.

When the CAPM assumptions hold, the market portfolio is efficient, so the tangency portfolio coincides with the market portfolio.

The SML is used to assess whether an individual asset is correctly priced according to the Capital Asset Pricing Model.