Investing in Risk-Free Securities

If a fraction \(x\) is invested in a risky portfolio \(P\) and the rest in Treasury bills, then:

\[ \mathbb{E}[R_C] = (1-x)r_f + x\mathbb{E}[R_P] = r_f + x\big(\mathbb{E}[R_P] - r_f\big) \]

\[ \operatorname{SD}(R_C) = x \operatorname{SD}(R_P) \]

So combinations of a risky portfolio and the risk-free asset lie on a straight line.

Because the risk-free return is constant and has zero covariance with the risky portfolio, both volatility and expected excess return scale proportionally with the weight invested in the risky portfolio.

Levered Portfolios

If \(x > 1\), the investor holds more than 100% in the risky portfolio and finances the additional exposure by borrowing at the risk-free rate.

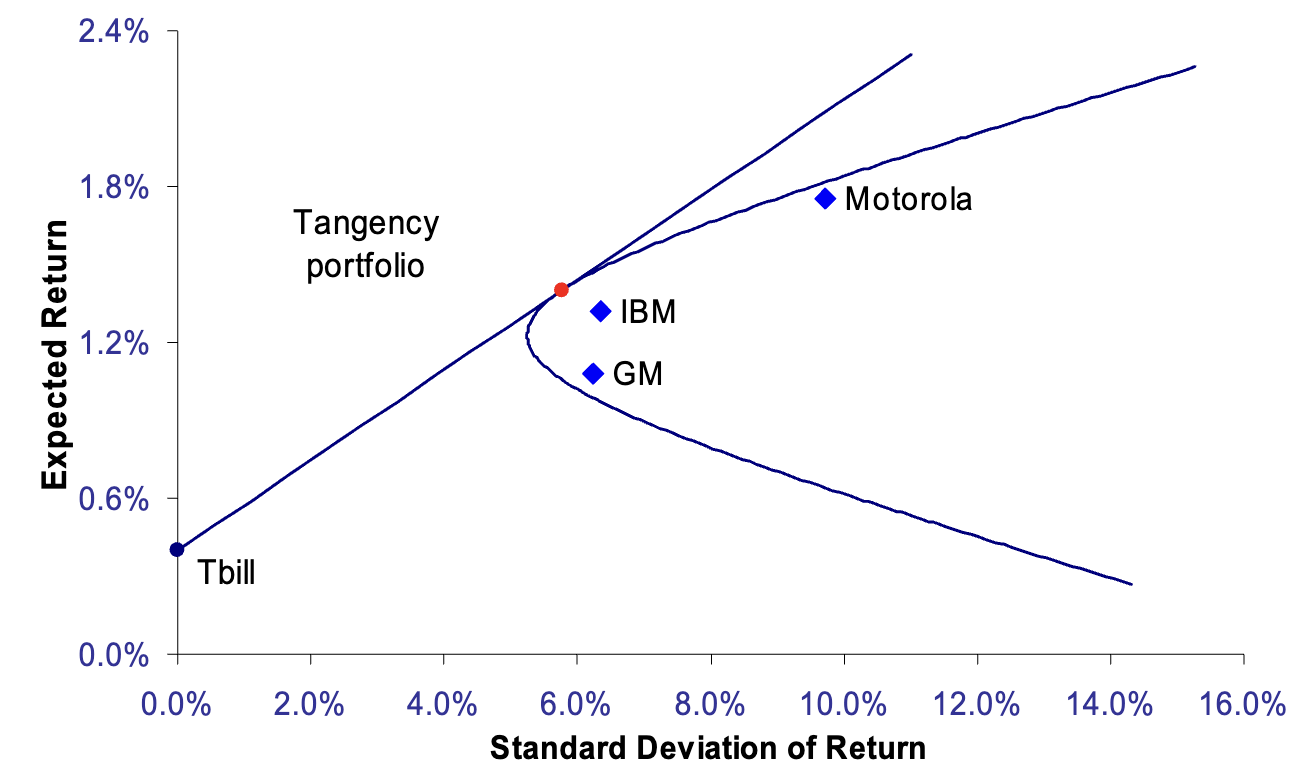

Tangency Portfolio

The tangency portfolio is the risky portfolio that generates the steepest possible capital allocation line when combined with the risk-free asset.

To earn the highest possible expected return for any level of volatility, we must find the portfolio that generates the steepest possible line when combined with the risk-free investment.

Investors may choose different mixes of the tangency portfolio and the risk-free asset, but they all hold the same portfolio of risky assets: the tangency portfolio.

Sharpe Ratio

\[ \text{Sharpe Ratio} = \frac{\mathbb{E}[R_P] - r_f}{\operatorname{SD}(R_P)} \]

The tangency portfolio has the highest Sharpe ratio of any feasible risky portfolio.

To improve a portfolio, a new investment must increase the portfolio's Sharpe ratio by offering enough extra expected return relative to the extra risk it adds.

In this sense, portfolio improvement requires more than a high stand-alone expected return; the new asset must also interact favorably with the assets already held through covariance.