MM Proposition II with Taxes

How \(V_L\) changes when the firm adds a project:

\[ \frac{\Delta V_L}{\Delta I} =\frac{(1-\tau_c)}{\rho}\frac{\Delta E(\widetilde{EBIT})}{\Delta I} +\tau_c\frac{\Delta B}{\Delta I}. \]

Decomposition shown in the slide:

\[ \frac{\Delta V_L}{\Delta I} =\frac{\Delta S^o}{\Delta I} +\frac{\Delta S^n}{\Delta I} +\frac{\Delta B^o}{\Delta I} +\frac{\Delta B^n}{\Delta I}. \]

Interpretation:

- \(\Delta S^o\): gain/loss for original shareholders,

- \(\Delta S^n\): value of new equity issued,

- \(\Delta B^o\): gain/loss for existing bondholders,

- \(\Delta B^n\): value of new debt issued.

With unchanged default risk for old debt, \(\Delta B^o=0\), and financing identity:

\[ \Delta I=\Delta S^n+\Delta B^n. \]

Hence:

\[ \frac{\Delta V_L}{\Delta I}=\frac{\Delta S^o}{\Delta I}+1. \]

Project acceptance for original shareholders requires:

\[ \frac{\Delta S^o}{\Delta I}>0 \iff \frac{\Delta V_L}{\Delta I}>1 \iff \frac{(1-\tau_c)}{\rho}\frac{\Delta E(\widetilde{EBIT})}{\Delta I} +\tau_c\frac{\Delta B}{\Delta I}>1. \]

Equivalent form (MM definition of WACC in the slide):

\[ \frac{(1-\tau_c)\,\Delta E(EBIT)}{\Delta I} >\rho\left(1-\tau_c\frac{\Delta B}{\Delta I}\right). \]

So a project creates value iff after-tax return exceeds the cost of capital.

Cost of Equity Capital Derivation

Cost of equity capital for the levered firm is the incremental return to equityholders per unit of new equity investment required by the project.

Total cash flow available for payment to debtholders and shareholders:

\[ NI+k_dD=EBIT(1-\tau_c)+k_dD\tau_c. \]

Now consider the change in each cash-flow component and divide by the new investment \(\Delta I\):

\[ \frac{\Delta NI}{\Delta I} +\frac{\Delta(k_dD)}{\Delta I} -\tau_c\frac{\Delta(k_dD)}{\Delta I} =(1-\tau_c)\frac{\Delta EBIT}{\Delta I}. \]

Substituting this operating-cash-flow identity into the levered-value expression gives:

\[ \frac{\Delta V_L}{\Delta I} =\frac{\dfrac{\Delta NI}{\Delta I} +\dfrac{\Delta(k_dD)}{\Delta I} -\tau_c\dfrac{\Delta(k_dD)}{\Delta I}}{\rho} +\tau_c\frac{\Delta B}{\Delta I}. \]

Collecting terms:

\[ \frac{\Delta V_L}{\Delta I} =\frac{\dfrac{\Delta NI}{\Delta I} +(1-\tau_c)\dfrac{\Delta(k_dD)}{\Delta I}}{\rho} +\tau_c\frac{\Delta B}{\Delta I}. \]

Using the decomposition of the change in levered value across the different claimholders:

\[ \frac{\Delta V_L}{\Delta I} =\frac{\Delta S^o+\Delta S^n}{\Delta I} +\frac{\Delta B}{\Delta I}. \]

Multiply both sides by \(\Delta I\):

\[ \Delta S^o+\Delta S^n+\Delta B =\frac{\Delta NI+(1-\tau_c)\Delta(k_dD)+\rho\tau_c\Delta B}{\rho}. \]

Subtract \(\Delta B\) from both sides:

\[ \Delta S^o+\Delta S^n =\frac{\Delta NI+(1-\tau_c)\Delta(k_dD)+\rho\tau_c\Delta B-\rho\Delta B}{\rho}. \]

For a perpetual risk-free debt stream, the market value of bonds satisfies:

\[ B=\frac{k_dD}{k_b}, \]

where \(k_b\) is the before-tax market-required rate of return for the risk-free stream. Therefore:

\[ k_b\Delta B=\Delta(k_dD). \]

Substituting this identity into the previous expression:

\[ \Delta S^o+\Delta S^n =\frac{\Delta NI+(1-\tau_c)k_b\Delta B+\rho\tau_c\Delta B-\rho\Delta B}{\rho}. \]

This yields:

\[ \rho(\Delta S^o+\Delta S^n)=\Delta NI-(1-\tau_c)(\rho-k_b)\Delta B. \]

Solving for the incremental return to equityholders:

\[ \frac{\Delta NI}{\Delta S^o+\Delta S^n} =\rho+(1-\tau_c)(\rho-k_b)\frac{\Delta B}{\Delta S^o+\Delta S^n}. \]

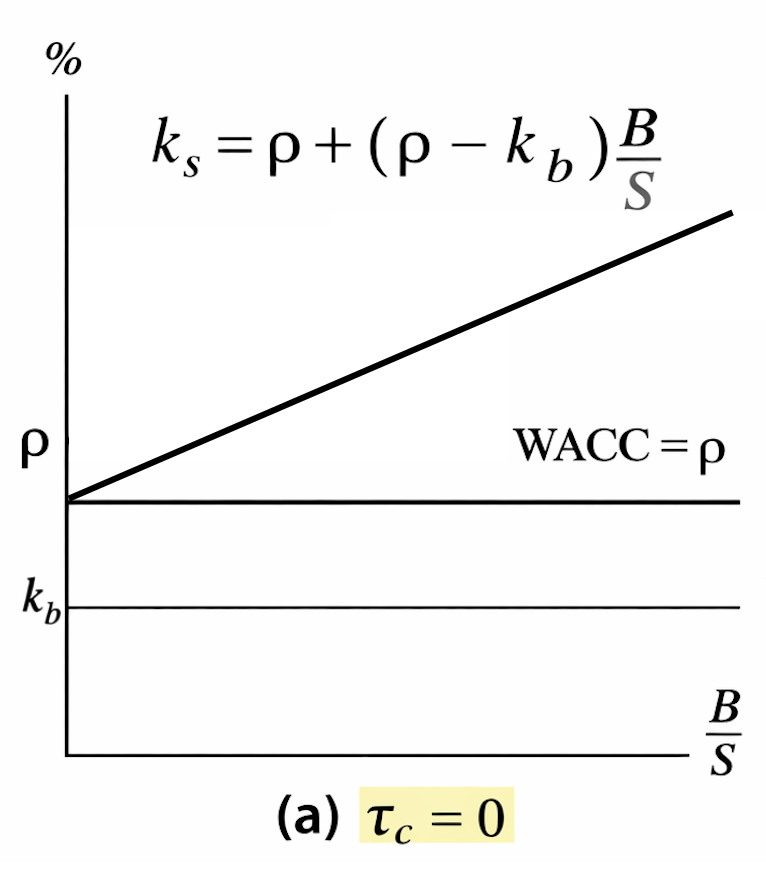

MM Proposition II (with taxes):

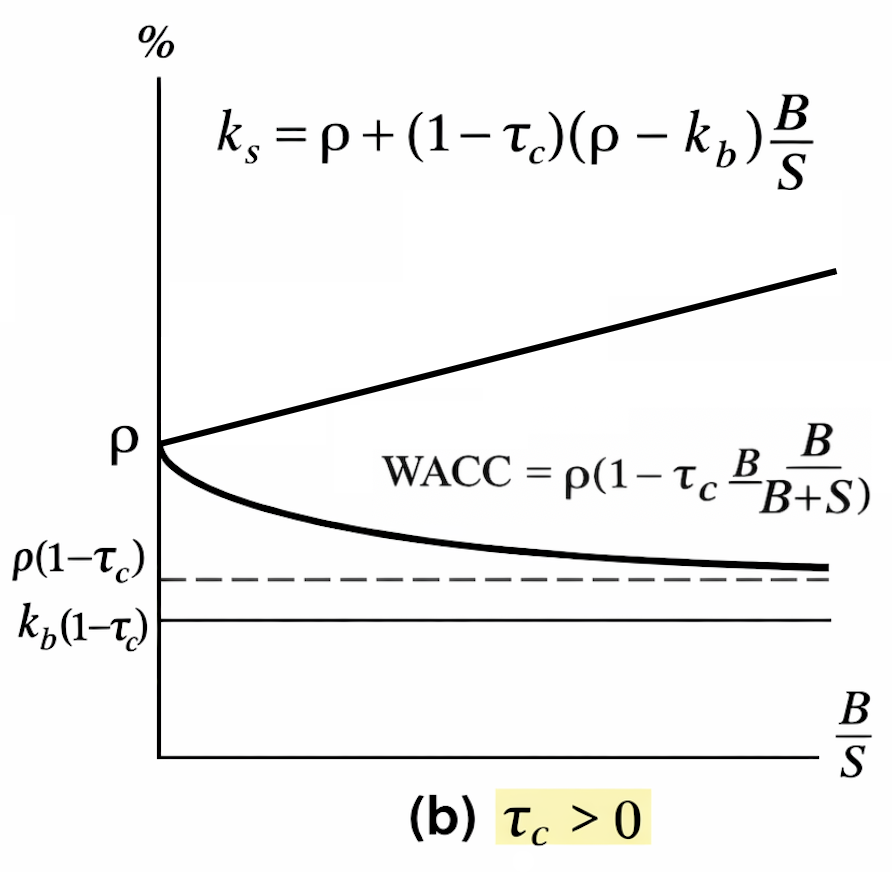

\[ k_s =\frac{\Delta NI}{\Delta S^o+\Delta S^n} =\frac{\Delta NI}{\Delta S} =\rho+(1-\tau_c)(\rho-k_b)\frac{\Delta B}{\Delta S^o+\Delta S^n} \approx \rho+(1-\tau_c)(\rho-k_b)\frac{B}{S}. \]

Key implications:

- Opportunity cost of capital to shareholders increases linearly with debt-to-equity (market value terms).

- With corporate taxes (\(\tau_c>0\)), WACC declines as leverage increases.

- In the no-tax case (\(\tau_c=0\)), WACC remains constant at \(\rho\).